Investments Overview

1693 Partners Fund

Coming off a record-setting year, the markets were primed for a setback; they just needed a spark. That spark came with the onset of inflation. While FY22 started out with reasonable optimism, as the calendar moved further into the year, the pendulum of investor sentiment shifted rapidly to a pessimistic viewpoint in the first quarter (and continuing into the second quarter of 2022), largely due to rising levels of inflation witnessed across most developed and emerging market economies.

As a result, as part of their explicit mandate, central banks became more aggressive in their monetary tightening plans to combat those inflation concerns. This caused interest rates to rise significantly during the year, putting downward pressure on equity valuations and upward pressure on fixed-income yields. The armed conflict in Eastern Europe and the prolonged COVID-19 lockdown measures in China continued to fuel supply chain bottlenecks, fanning the flames of the investor pessimism.

All told, the MSCI AC World Index, an index that measures global equity returns, returned a negative 15.4% for the fiscal year. Normally, fixed-income investment would provide some ballast to a portfolio facing such hostility in the equity markets, but that was not the case this fiscal year. Indeed, the Bloomberg Aggregate Bond index returned a negative 10.3%.

While the 1693 Partners Fund was able to mitigate much of the downside experienced in public markets during the fiscal year, nonetheless the portfolio did produce a modestly negative return of 3.5% for the one-year period. However, the Fund significantly outperformed the Policy benchmark, which lost 13.7% over the same time period.

As I continue to point out, it is not what happens in any one-year period that defines a successful (or unsuccessful) investment strategy; the best gauge is reviewing longer-term results. I am pleased to report those numbers continue to be strong and comfortably ahead of the benchmark. Please see the table below detailing the longer-term results for the portfolio. Assets in the Partners Fund ended the fiscal year at $898.8 million.

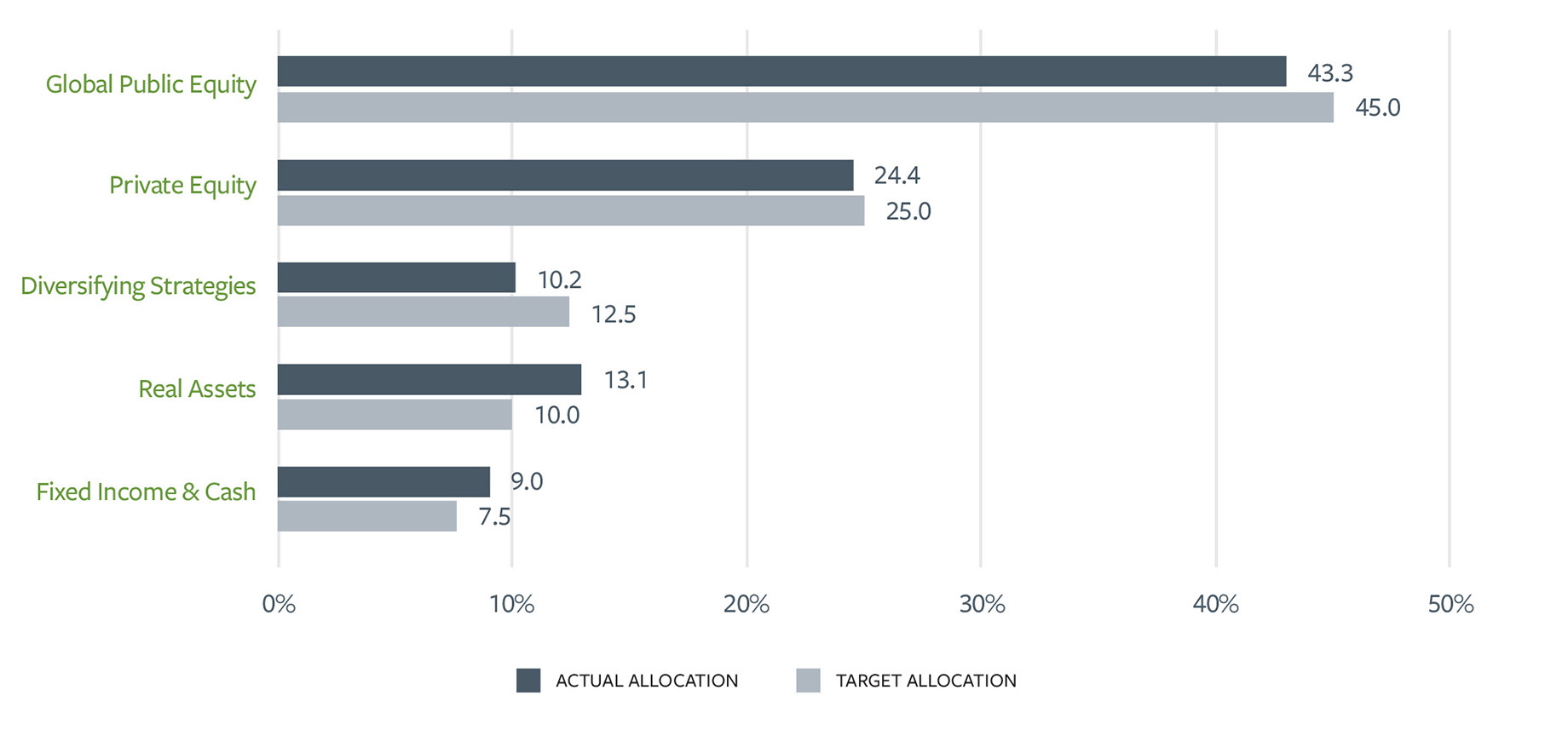

1693 Partners Fund Actual versus Target Allocations

As of June 30, 2022

The exhibit below highlights the Partners Fund asset allocation as of the end of FY22. On balance, the Partners Fund is hovering around the target allocations among the various broad asset classes with a modest underweight to Global Public Equities and modest overweighting to Real Assets.

Fiscal Year 2022 Investments Performance

Given the hostile macro environment, the portfolio’s investments in Global Public Equities returned negative 19.1% for the fiscal year, compared to the MSCI All-Country World, its benchmark, which produced a negative 15.4%. As of June 30, 2022, Global Public Equities represented 43.3% of the aggregate portfolio. In terms of geography, the best performing asset class was the U.S. The portfolio’s U.S.-focused investments with a weighting of ~22% returned a negative 16.5%, compared to a negative 13.9% return for the Russell 3000 index.

Small cap exposure and idiosyncratic manager performance led to the unfavorable result in the fiscal year. While short-term performance has been less than optimal, we are confident that our managers will deliver the required alpha in the long term.

Developed International Equities, accounting for 17.1% of the portfolio, returned a negative 20.7% trailing the MSCI EAFE benchmark return of negative 17.8%. From a geographic perspective, while the Emerging Markets allocation was the most challenged from an absolute return point of view (negative 25% for the fiscal year), it did manage to slightly outperform its benchmark, the MSCI Emerging Markets Index. The portfolio continues to have a modest weighting (4.2%) invested in emerging market equities.

Private Equity, which includes venture capital, buyout and growth equity investments in private companies, had the second largest allocation in the portfolio at 24.4% of assets. The portfolio saw another year of strong gains, appreciating in value by 21.9% for the fiscal year. Given the volatility in public equity markets and the lag effect of private market valuations, we expect to see some potential decline in value in FY23, although it is too early to definitively say that will be the case.

As mentioned previously, the investment environment for traditional equities and fixed-income securities was challenging in the year. Having exposure to strategies that can potentially diversify investment risks, generate investment returns, and mitigate downside volatility proved to be compelling this year. The Partners Fund’s exposure to these types of investments — we categorize them as Diversifying Strategies — summed to 10.2% of the overall portfolio. This allocation includes investments in private credit, specialty finance lending, multi-strategy hedge funds, and non-correlated strategies including cash flow-based royalty investments, and it produced in aggregate a negative 2.9% for the fiscal year. These investments provided the portfolio some downside protection this fiscal year.

Fixed-Income assets within the portfolio remain modest, 3.6% of the portfolio. As mentioned, central banks around the world began an aggressive interest rate increase campaign during the fiscal year. This provided a significant headwind to traditional fixed-income investments, as yields and prices are inversely related. However, credit spreads remained stable in the face of rising short-term risk-free rates. It is still too early to know when the end of the interest rate hike cycle will occur; the key to this will be whether central banks can get inflation under control without damaging the economy meaningfully.

We remain cautious with the exposure to traditional fixed income, although we are beginning to see signs of attractive opportunities on a risk-adjusted basis in traditional fixed income. This is a statement we have not been able to make in a long time.

Finally, Real Assets, with a 13.1% weighting, had meaningful exposure to real estate. In FY22, the Real Asset portfolio returned a positive 27.3% while the benchmark returned a positive 8.3%. The portfolio was fortunate to have exposure to certain sectors of the real estate market that produced attractive absolute and relative returns. The allocation’s investments in energy infrastructure also contributed meaningfully to this year’s overall Real Assets results.

Brian Hiestand

Chief Executive Officer & Chief Investment Officer

1693 Management Company, LLC